6 Recurrent Neural Networks

6.1 Overview

Feed-forward neural networks are flexible nonlinear maps from an input vector to an output, but they do not have a built-in state variable. If we want to use them for time-series forecasting, we usually have to create lagged inputs manually, such as \((y_{t-1}, y_{t-2}, \ldots, y_{t-p})\). That approach is often useful, but it fixes the memory length \(p\) in advance and treats temporal dependence as a feature-engineering problem.

Recurrent neural networks (RNNs) instead maintain a hidden state that is updated as new observations arrive. This makes them closer in spirit to econometric models with recursively updated states, such as ARMA, state-space, or GARCH-type models. The key difference is that the update function is learned from data and can be nonlinear and high-dimensional.

This chapter introduces the basic RNN architecture in a forecasting setting, interprets it through an econometric state-variable lens, and then explains the central difficulty of standard RNNs: vanishing gradients. The basic recurrent architecture is closely associated with Elman (1990), while training through an unrolled sequence uses the backpropagation ideas of Rumelhart, Hinton, and Williams (1986) and backpropagation through time as described by Werbos (1990). The vanishing-gradient difficulty is analyzed in Bengio, Simard, and Frasconi (1994). That difficulty is the main reason why the next chapter moves to Long Short-Term Memory (LSTM) networks.

6.2 Roadmap

- We first define the forecasting setup and the information-set problem that RNNs are meant to address.

- We contrast a lagged feed-forward network with a recurrent state update.

- We introduce the RNN equations, parameter sharing, and the unrolled computational graph.

- We connect RNNs to econometric state-variable models such as GARCH.

- We discuss deterministic versus probabilistic outputs for forecasting applications.

- We finish with backpropagation through time, the vanishing gradient problem, and the motivation for LSTMs.

6.3 Forecasting Setup and the Information Set

Suppose we want to forecast a scalar outcome \(y_{t+1}\) using information available at time \(t\). Let \(\mathcal{F}_t\) denote that information set. In a macroeconomic or financial application, \(\mathcal{F}_t\) may contain past values of the target variable, lagged predictors, realized returns, volatility measures, survey variables, text-based indicators, and other signals known at the forecast origin.

A lagged feed-forward network uses a fixed window of this information, for example

\[ \hat{y}_{t+1} = f_\theta(y_t, y_{t-1}, \ldots, y_{t-p}, \mathbf{x}_t, \mathbf{x}_{t-1}, \ldots, \mathbf{x}_{t-p}). \]

This is a reasonable baseline. It is close to how econometricians build distributed-lag or autoregressive forecasting models. The limitation is that the lag length \(p\) must be chosen before estimation, and the model does not update an internal state as new observations arrive.

An RNN replaces the fixed lag window by a recursively updated summary:

\[ \mathbf{h}_t = \text{summary}_\theta(\mathbf{x}_1, \ldots, \mathbf{x}_t). \]

The hidden state \(\mathbf{h}_t\) is not observed and should not be interpreted too literally. It is a learned vector summary of the past that is useful for prediction.

For this course, the useful analogy is: an RNN is a nonlinear state-update model. Like a state-space model or a GARCH recursion, it carries information forward through a state variable. Unlike those classical models, the state update is not chosen by theory in a low-dimensional parametric form; it is learned as part of a neural network.

6.4 From a Lagged FNN to a Recurrent State

An RNN replaces the fixed lag window by carrying a hidden state across time steps. At each step, the network updates the hidden state from the current input and the previous state, so all earlier observations enter the prediction through the current state.

A feed-forward network with lagged inputs can approximate nonlinear autoregressive relationships, but it treats the chosen lag vector as the full input. If the relevant history changes over time or spans many periods, this fixed-window approach becomes limited.

An RNN uses the same update rule at every time step. At time \(t\), it takes the current input \(\mathbf{x}_t\) and the previous hidden state \(\mathbf{h}_{t-1}\) and produces a new hidden state \(\mathbf{h}_t\). This creates a recursive representation of the past:

\[ \mathbf{h}_t = g_\theta(\mathbf{h}_{t-1}, \mathbf{x}_t). \]

This state can then be used to produce a forecast, classification probability, or distributional parameter:

\[ \hat{y}_{t+1} = q_\theta(\mathbf{h}_t). \]

The essential point is that the model learns both the update rule and the predictive mapping.

6.5 RNN Architecture and Notation

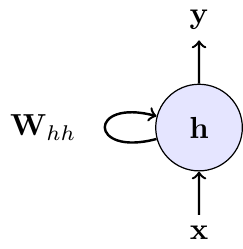

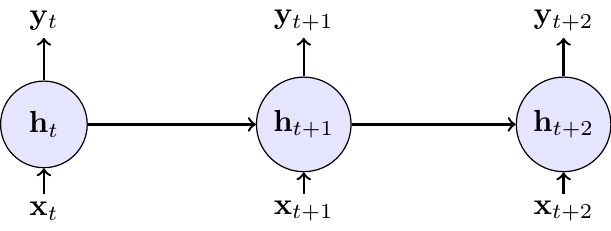

The recurrence can be visualized in two ways: a compact form with a self-loop, representing the recurrence, and an “unrolled” form, which shows the flow of information through time.

The left panel in Figure 6.1 shows the compact representation: a recurrent link feeds the previous hidden state back into the model. The right panel shows the same model unrolled through time. Unrolling is mainly a computational device for training; it does not mean that the model has different parameters at different dates.

At each time step \(t\), define:

- \(\mathbf{x}_t \in \mathbb{R}^{D}\): The input vector at the current time step (e.g., today’s stock returns and trading volume).

- \(\mathbf{h}_{t-1} \in \mathbb{R}^{H}\): The hidden state from the previous time step, which acts as the network’s memory of the past.

- \(\mathbf{h}_t \in \mathbb{R}^{H}\): The new hidden state, calculated by combining the current input \(\mathbf{x}_t\) with the previous state \(\mathbf{h}_{t-1}\).

- \(\mathbf{y}_t \in \mathbb{R}^{O}\): The output at the current time step (e.g., the prediction for tomorrow’s volatility), produced from the current hidden state.

The update equations are:

\[ \begin{align} \mathbf{h}_t &= g(\mathbf{W}_{hh}\mathbf{h}_{t-1} + \mathbf{W}_{xh}\mathbf{x}_t + \mathbf{b}_h) \quad &\text{(Update memory)} \\ \mathbf{y}_t &= \mathbf{W}_{hy}\mathbf{h}_t + \mathbf{b}_y \quad &\text{(Produce output)} \end{align} \]

with \(\mathbf{h}_0\) fixed by convention, typically \(\mathbf{h}_0 = \mathbf{0}\), since the state recursion is otherwise undefined at \(t=1\), and with the following parameters:

- \(\mathbf{W}_{hh} \in \mathbb{R}^{H \times H}\) (hidden-to-hidden weights)

- \(\mathbf{W}_{xh} \in \mathbb{R}^{H \times D}\) (input-to-hidden weights)

- \(\mathbf{W}_{hy} \in \mathbb{R}^{O \times H}\) (hidden-to-output weights)

- \(\mathbf{b}_h \in \mathbb{R}^{H}\), \(\mathbf{b}_y \in \mathbb{R}^{O}\) (bias terms)

These are collectively \(\theta = \{\mathbf{W}_{hh}, \mathbf{W}_{xh}, \mathbf{W}_{hy}, \mathbf{b}_h, \mathbf{b}_y\}\), the parameters that the generic maps \(f_\theta\), \(g_\theta\), and \(q_\theta\) introduced above stand for.

RNN implementations typically use \(\tanh\) as the activation \(g\), because it is bounded and zero-centered.

In the generic notation above, \(\mathbf{y}_t\) denotes the output produced after seeing \(\mathbf{x}_t\). In a one-step-ahead forecasting application, we would often interpret that output as \(\hat{y}_{t+1}\) or as parameters of the predictive distribution for \(y_{t+1} \mid \mathcal{F}_t\).

Key Properties

- Parameter sharing: The same weight matrices (\(\mathbf{W}_{hh}, \mathbf{W}_{xh}, \mathbf{W}_{hy}\)) and biases are used at every time step. The total parameter count is therefore independent of sequence length, so the same network can be applied to sequences of different lengths.

- Memory: The hidden state \(\mathbf{h}_t\) carries information from past inputs forward, so observations at \(t-k\) for \(k\geq 1\) can still influence \(\hat y_{t+1}\) through the state.

6.6 Econometric State-Variable Interpretation

An RNN can be viewed as a flexible nonlinear generalization of classical time-series models with recursively updated states. A useful benchmark is the GARCH model of Bollerslev (1986).

In the GARCH(1,1) model, the return at \(t\) is decomposed as \(r_t = \mu_t + \varepsilon_t\) where \(\mu_t\) is the conditional mean and \(\varepsilon_t\) is the innovation. The conditional variance of \(\varepsilon_t\) then follows the recursion

\[ \sigma_t^2 = \omega + \alpha \varepsilon_{t-1}^2 + \beta \sigma_{t-1}^2, \]

where \(\omega>0\), \(\alpha,\beta\geq 0\), and \(\alpha+\beta<1\) for covariance stationarity. The state is \(\sigma_{t-1}^2\), and the update is linear in the lagged squared innovation and the lagged variance.

An RNN-style volatility model could instead use

\[ \begin{align} \mathbf{h}_t &= \tanh(\mathbf{W}_{hh}\mathbf{h}_{t-1} + \mathbf{W}_{xh}\mathbf{x}_t + \mathbf{b}_h) \\ \sigma_{t+1}^2 &= \text{softplus}(\mathbf{W}_{hy}\mathbf{h}_t + \mathbf{b}_y), \end{align} \]

where \(\mathbf{x}_t\) might contain lagged returns, squared returns, realized volatility measures, or macro-financial predictors known at time \(t\). The hidden state \(\mathbf{h}_t\) is a high-dimensional vector that learns a nonlinear summary of the relevant history. The softplus transformation ensures a positive variance forecast.

The analogy has clear limits. In a GARCH model, the conditional variance has a direct structural interpretation within a specified conditional distribution. In a standard RNN, the hidden state is a predictive representation, not a structural object. It becomes a probabilistic econometric model only after we specify how the output maps into a conditional distribution or likelihood.

The hidden state \(\mathbf{h}_t\) plays a role similar to a state vector in a state-space model or a volatility state in GARCH. The difference is that its components are learned predictive features, not parameters with a direct one-to-one econometric interpretation.

6.7 Outputs and Loss Functions

The output layer determines what kind of forecasting object the RNN produces. For a conditional mean forecast, we can use a linear output

\[ \hat{y}_{t+1} = \mathbf{W}_{hy}\mathbf{h}_t + \mathbf{b}_y \]

and train by minimizing squared loss. For a binary event, such as recession prediction, we can pass the output through a sigmoid and train with cross-entropy. For a probabilistic forecast, the output should parameterize a distribution. For example, for demeaned returns \(\varepsilon_{t+1}\):

\[ \varepsilon_{t+1} \mid \mathcal{F}_t \sim \mathcal{N}(0, \sigma_{t+1}^2), \qquad \sigma_{t+1}^2 = \text{softplus}(\mathbf{W}_{hy}\mathbf{h}_t + \mathbf{b}_y). \]

This distinction matters in econometrics. A deterministic RNN trained by squared loss gives a point forecast. A distributional RNN trained by negative log-likelihood gives a predictive distribution that can be evaluated with the scoring rules from the predictive-distribution chapter.

For time-series applications, \(\mathbf{x}_t\) and \(\mathbf{h}_t\) must only use information available at the forecast origin. The recurrent architecture does not remove the usual econometric concern about look-ahead bias, revised macroeconomic data, publication lags, or temporal leakage in validation.

If a macroeconomic predictor is published with a one-month delay and later revised, what should be included in \(\mathcal{F}_t\) when training an RNN for real-time forecasting?

\(\mathcal{F}_t\) should contain only the real-time data vintage available at the forecast origin. With a one-month publication delay, the current-month value is not available, and later revisions are also unavailable. The RNN input should therefore use the last released vintage and respect the release calendar, rather than the revised historical series that becomes available only later.

6.8 Training Through Time

Training an RNN raises a problem absent from feed-forward networks: because the same weight matrices (\(\mathbf{W}_{hh}, \mathbf{W}_{xh}\)) are applied at every time step, their gradient is the sum of contributions from every time step. The algorithm that handles this is Backpropagation Through Time (BPTT).

The core idea of BPTT is to unroll the network through time, as shown in Figure 6.1. This conceptually transforms the RNN into a deep feed-forward network where each time step becomes a layer, but with the critical constraint that the weights are shared across all layers. Once unrolled, standard backpropagation can be applied.

For clarity, the chapter specializes to a single terminal loss \(L_T = \ell(\mathbf{y}_T, y_T)\) evaluated at the terminal step \(T\); the sequence-to-sequence case with per-step losses \(\sum_{t} \ell(\mathbf{y}_t, y_t)\) sums analogously over the terms below. If the loss is evaluated at the final time \(T\), the gradient for a recurrent weight matrix is the sum of its contributions across time. For example, the gradient with respect to \(\mathbf{W}_{hh}\) can be written schematically as:

\[ \frac{\partial L_T}{\partial \mathbf{W}_{hh}}=\sum_{t=1}^{T}\frac{\partial L_T}{\partial \mathbf{h}_t}\frac{\partial \mathbf{h}_t}{\partial \mathbf{W}_{hh}} \]

The term \(\frac{\partial L_T}{\partial \mathbf{h}_t}\) captures how an adjustment to the hidden state at an early time \(t\) affects the final loss at time \(T\). This requires propagating the gradient backwards through every intermediate step, leading to a long product of Jacobian matrices:

\[ \frac{\partial \mathbf{h}_t}{\partial \mathbf{h}_k} = \prod_{i=k+1}^{t} \frac{\partial \mathbf{h}_i}{\partial \mathbf{h}_{i-1}} = \prod_{i=k+1}^{t} \mathbf{W}_{hh}^{\top}\,\operatorname{diag}\big(g'(\mathbf{z}_i)\big) \]

where \(g'\) is the derivative of the activation function (e.g., \(\tanh'\)) and \(\mathbf{z}_i = \mathbf{W}_{hh}\mathbf{h}_{i-1} + \mathbf{W}_{xh}\mathbf{x}_i + \mathbf{b}_h\) is its pre-activation input at step \(i\). The detailed derivations for a one-dimensional hidden state can be found in a self-study exercise at the end of this section.

6.9 Vanishing Gradients as the Main Limitation

The long product of Jacobians is the source of the vanishing gradient problem. If the norms of the recurrent weight matrix and the activation derivatives are, on average, less than one, repeated multiplication causes the gradient signal to shrink exponentially as it propagates backwards through time. Consequently, contributions from early time steps (\(t \ll T\)) become so small that they are effectively zero.

For econometric forecasting, this is the central limitation of a plain RNN. The model may have a recursive state, but the training algorithm may still fail to learn long-run dependence because the relevant gradients disappear before they can influence the parameters. In practice, parameter updates become dominated by recent observations, which makes the model behave more like a short-memory nonlinear autoregression than a robust long-memory sequence model.

Plain RNNs are rarely the best architecture for macroeconomic or financial sequences. Their value in this chapter is conceptual: they expose the structural problem that learning long-run dependence requires gradient signal across many time steps. LSTMs address this by modifying the state update with gates and a cell state that preserve information more reliably.

6.10 Summary

- A recurrent neural network augments a feed-forward network with a hidden state that is updated over time.

- In forecasting applications, the hidden state is a learned summary of the information set available at the forecast origin.

- Econometrically, an RNN can be interpreted as a flexible nonlinear state-update model, similar in spirit to GARCH or state-space recursions but less tightly specified.

- A standard RNN output is deterministic unless we combine it with a probabilistic output layer and a likelihood.

- Training uses backpropagation through time, which applies the chain rule to an unrolled sequence of shared-parameter hidden states.

- The main limitation of plain RNNs is the vanishing gradient problem: early time steps can have almost no influence on parameter updates for long sequences.

- The vanishing gradient problem is the main conceptual bridge to LSTM networks in the next chapter.

- Treating an RNN hidden state as directly interpretable in the same way as a scalar GARCH variance or an AR state.

- Forgetting that a deterministic RNN forecast is not automatically a full predictive distribution.

- Randomly shuffling time-series observations before training or evaluation, thereby destroying the temporal information structure or leaking future information.

- Assuming that a plain RNN can learn very long-run dependence just because the hidden state is recursively updated.

- Confusing the unrolled computational graph used for training with a model that has different parameters at each time step; standard RNNs share parameters over time.

6.11 Exercises

In this exercise, we examine the vanishing gradient problem in RNNs. Consider a simple RNN with one-dimensional hidden state \(h_t = \tanh(W_h h_{t-1} + W_x x_t + b)\) and loss \(L_T\) at the final time step \(T\).

Tasks:

- Derive the gradient formula for backpropagation through time. Using the chain rule, derive the expression for \(\frac{\partial L_T}{\partial W_h}\). Show that it involves the term \(\frac{\partial h_T}{\partial h_t}\) for each time step \(t = 1, 2, \ldots, T\) and express it as a product of derivatives.

- Prove gradient vanishing conditions. Show that \(\left |\frac{\partial h_T}{\partial h_t}\right | \leq | W_h |^{T-t}\) and explain why this leads to exponentially vanishing gradients when \(|W_h | < 1\).

- Analyze learning implications. Explain why vanishing gradients prevent RNNs from learning long-term dependencies, including the effect on parameter updates for early time steps and typical sequence length limitations.

Technically at exam level. However, it’s hard to come up with variations of this exercise. Hence, any exam question would be very close to this setup.

For part 1, use the chain rule to express \(\frac{\partial L_T}{\partial W_h}\). Remember that the weight \(W_h\) affects the loss through its influence on all hidden states from time 1 to \(T\).

The key insight is that \(\frac{\partial L_T}{\partial W_h} = \sum_{t=1}^T \frac{\partial L_T}{\partial h_T} \frac{\partial h_T}{\partial h_t} \frac{\partial h_t}{\partial W_h}\).

For the product of derivatives, think about how \(h_T\) depends on \(h_t\) through the chain: \(h_t \to h_{t+1} \to h_{t+2} \to \cdots \to h_T\).

For part 2, you need to bound the absolute value of a product of derivatives. Use the property that \(|ab| = |a||b|\).

Each derivative \(\frac{\partial h_k}{\partial h_{k-1}}\) involves both the weight \(W_h\) and the derivative of the activation function. What’s the maximum value of \(\tanh'(z)\)?

For part 3, think about what happens to the gradient terms \(\frac{\partial L_T}{\partial W_h}\) when the \(\frac{\partial h_T}{\partial h_t}\) terms become very small for early time steps. How does this affect which time steps contribute most to parameter updates?

The goal is to find \(\frac{\partial L_T}{\partial W_h}\). The key challenge is that the weight \(W_h\) is used at every time step, so its influence on the final loss \(L_T\) is the sum of its influence through each step.

The final loss \(L_T\) is a function of the last hidden state, \(h_T\). But \(h_T\) is a function of \(h_{T-1}\) and \(W_h\). And \(h_{T-1}\) is a function of \(h_{T-2}\) and \(W_h\), and so on. This means that the final loss \(L_T\) is ultimately a function of \(W_h\) through its influence on every single hidden state:

\(L_T = f(h_T(h_{T-1}(...h_1(W_h)...), W_h), W_h)\)

Since \(W_h\) contributes to the final loss through all these paths, we have by the multivariate chain rule:

\[ \frac{\partial L_T}{\partial W_h} = \sum_{t=1}^T \frac{\partial L_T}{\partial h_t} \frac{\partial h_t}{\partial W_h} \]

Calculating the Direct Influence

The term \(\frac{\partial h_t}{\partial W_h}\) represents the direct influence of \(W_h\) on \(h_t\) at a single time step. From the RNN equation \(h_t = \tanh(W_h h_{t-1} + W_x x_t + b)\), this is straightforward:

\[ \frac{\partial h_t}{\partial W_h} = \tanh'(W_h h_{t-1} + W_x x_t + b) \cdot h_{t-1} \]

Calculating the Indirect Influence (The Chain Rule Through Time)

The term \(\frac{\partial L_T}{\partial h_t}\) is more complex. It measures how a change in an early hidden state \(h_t\) propagates all the way to the end to affect the final loss \(L_T\). We must use the chain rule through the sequence of hidden states:

\[ \frac{\partial L_T}{\partial h_t} = \frac{\partial L_T}{\partial h_T} \frac{\partial h_T}{\partial h_{T-1}} \frac{\partial h_{T-1}}{\partial h_{T-2}} \cdots \frac{\partial h_{t+1}}{\partial h_t} = \frac{\partial L_T}{\partial h_T} \prod_{k=t+1}^T \frac{\partial h_k}{\partial h_{k-1}} \]

This long chain of derivatives is the core of backpropagation through time.

Now we can write the full expression for the gradient. Substituting our product form back into the sum at the beginning, we get

\[ \frac{\partial L_T}{\partial W_h} = \sum_{t=1}^T \underbrace{\left( \frac{\partial L_T}{\partial h_T} \prod_{k=t+1}^T \frac{\partial h_k}{\partial h_{k-1}} \right)}_{\frac{\partial L_T}{\partial h_t}} \underbrace{\left( \frac{\partial h_t}{\partial W_h} \right)}_{\text{direct effect}} \]

This formula explicitly shows that the gradient contribution from each time step \(t\) involves a product of terms that bridges the time gap from \(t\) to \(T\).

Each derivative in the product has the form:

\[ \frac{\partial h_k}{\partial h_{k-1}} = \tanh'(W_h h_{k-1} + W_x x_k + b) \cdot W_h \]

Since \(\tanh'(z) = 1 - \tanh^2(z) \leq 1\), its value is always between 0 and 1. We can bound the absolute value of the derivative:

\[ \left|\frac{\partial h_k}{\partial h_{k-1}}\right| = |\tanh'(\cdot)| \cdot |W_h| \leq 1 \cdot |W_h| = |W_h| \]

The key term \(\frac{\partial h_T}{\partial h_t}\) for \(t < T\) represents the product of derivatives through time:

\[ \left|\frac{\partial h_T}{\partial h_t}\right| = \left|\prod_{k=t+1}^T \frac{\partial h_k}{\partial h_{k-1}}\right| \leq |W_h|^{T-t} \]

Exponential vanishing: When \(|W_h| < 1\), we have \(|W_h|^{T-t} \to 0\) exponentially as the time gap \((T-t)\) increases. This proves the exponential decay of gradient magnitudes.

The bound above is the scalar \(H=1\) case in which the recurrent weight \(W_h\) is a single real number. For a multi-dimensional hidden state (\(H>1\)), \(W_h\) is a square matrix and the per-step bound uses the spectral norm \(\|W_h\|_2\) (the largest singular value):

\[ \left\|\frac{\partial h_T}{\partial h_t}\right\|_2 \le \prod_{k=t+1}^{T} \|W_h\|_2 \cdot \|\mathrm{diag}(g'(\mathbf z_k))\|_2 \le \|W_h\|_2^{T-t}. \]

The asymptotic rate of decay is governed by the spectral radius \(\rho(W_h) = \max_i |\lambda_i(W_h)|\), and the two coincide when \(W_h\) is normal (e.g., symmetric). The qualitative conclusion is the same as in the scalar case: when the recurrent dynamics are contractive, gradients decay exponentially in \(T-t\).

The exponential decay has three critical effects on learning:

Dominated parameter updates: Since \(\frac{\partial L_T}{\partial W_h} = \sum_{t=1}^T \frac{\partial L_T}{\partial h_T} \frac{\partial h_T}{\partial h_t} \frac{\partial h_t}{\partial W_h}\), when \(\frac{\partial h_T}{\partial h_t}\) becomes exponentially small for early \(t\), the gradient sum becomes dominated by recent time steps (large \(t\)).

Loss of long-term information: The network cannot learn patterns where important information at time \(t\) influences the loss at time \(T\) when \(T-t\) is large, because the gradient signal carrying this information becomes negligibly small.

Practical sequence limitations: The bound does not imply a universal cutoff such as a fixed maximum number of lags. It says that, unless the recurrent dynamics are unusually well conditioned, the gradient contribution of distant observations decays exponentially with the gap \(T-t\). In practice this makes plain RNNs unreliable for long-run dependence without architectural or training modifications.

The fundamental issue is that learning requires non-negligible gradients to update parameters, but the exponential decay ensures that distant time steps contribute virtually nothing to parameter updates.

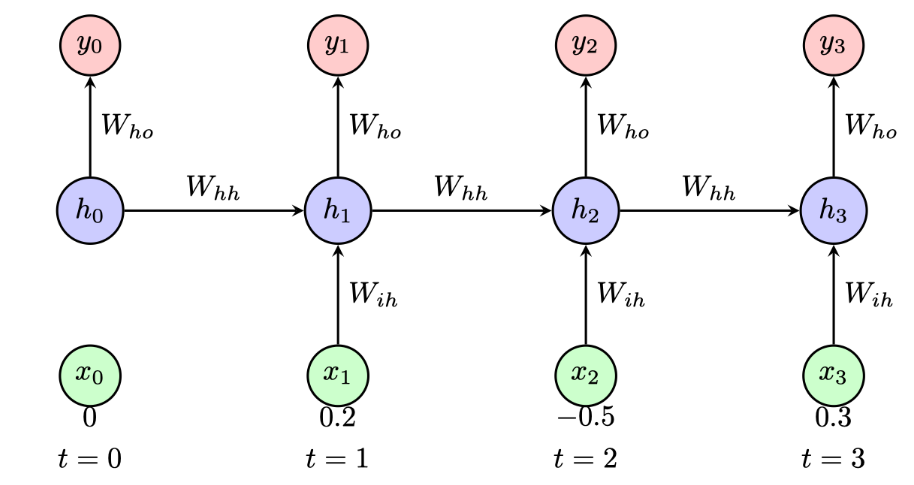

Consider a simple RNN with a single hidden unit processing a sequence of length 3. The RNN has the following parameters:

- Weight for input-to-hidden: \(W_{ih} = 0.5\)

- Weight for hidden-to-hidden: \(W_{hh} = 0.8\)

- Bias for hidden unit: \(b_h = 0.1\)

- Weight for hidden-to-output: \(W_{ho} = 1.2\)

- Bias for output: \(b_o = 0.0\)

The activation function for the hidden unit is \(\tanh\) and the output is linear (no activation). Given the input sequence \(\mathbf{x} = [0.2, -0.5, 0.3]\) and the initial hidden state \(h_0 = 0\):

- Compute the hidden state \(h_1\) and output \(y_1\) at time step \(t = 1\).

- Compute the hidden state \(h_2\) and output \(y_2\) at time step \(t = 2\).

- Compute the hidden state \(h_3\) and output \(y_3\) at time step \(t = 3\).

- The second input \(x_2 = -0.5\) is large and negative, yet \(h_2 \approx 0.008\) is nearly zero. Explain why the hidden-to-hidden weight \(W_{hh} = 0.8\) partially offsets the current input, and discuss what this implies for the vanishing-gradient problem identified in Exercise 6.1: does the hidden state at \(t=2\) carry much information about the input at \(t=1\)?

Exam level.

Work through each time step sequentially using \(h_t = \tanh(W_{ih} x_t + W_{hh} h_{t-1} + b_h)\) and \(y_t = W_{ho} h_t + b_o\). Use \(\tanh(0.2) \approx 0.197\), \(\tanh(0.008) \approx 0.008\), and \(\tanh(0.256) \approx 0.251\).

Part 1: \(t = 1\)

\[ \begin{aligned} h_1 &= \tanh(0.5 \cdot 0.2 + 0.8 \cdot 0 + 0.1) = \tanh(0.2) \approx 0.197 \\ y_1 &= 1.2 \cdot 0.197 \approx 0.236 \end{aligned} \]

Part 2: \(t = 2\)

\[ \begin{aligned} h_2 &= \tanh(0.5 \cdot (-0.5) + 0.8 \cdot 0.197 + 0.1) \\ &= \tanh(-0.25 + 0.158 + 0.1) = \tanh(0.008) \approx 0.008 \\ y_2 &= 1.2 \cdot 0.008 \approx 0.010 \end{aligned} \]

Part 3: \(t = 3\)

\[ \begin{aligned} h_3 &= \tanh(0.5 \cdot 0.3 + 0.8 \cdot 0.008 + 0.1) \\ &= \tanh(0.15 + 0.006 + 0.1) = \tanh(0.256) \approx 0.251 \\ y_3 &= 1.2 \cdot 0.251 \approx 0.301 \end{aligned} \]

Part 4: Information retention and the vanishing gradient

At \(t = 2\), the large negative input \(W_{ih} x_2 = 0.5 \times (-0.5) = -0.25\) is almost exactly offset by the memory term \(W_{hh} h_1 = 0.8 \times 0.197 = 0.158\) and the bias \(b_h = 0.1\), giving a pre-activation near zero and thus \(h_2 \approx 0\). As a result, almost all information about \(x_1\) that was stored in \(h_1\) has been overwritten.

This connects directly to the vanishing gradient in Exercise 6.1. The gradient of the loss at \(T\) with respect to \(h_1\) passes through the factor \(W_{hh} \cdot \tanh'(\cdot)\). Since \(\tanh'(z) \leq 1\) and \(W_{hh} = 0.8\), each step multiplies the gradient by at most \(0.8\). Over many steps this product decays toward zero, so the network cannot learn to preserve information from \(t = 1\) through many subsequent time steps. The near-zero \(h_2\) in this example is a concrete illustration: the hidden state at \(t = 2\) carries essentially no memory of \(x_1\).